|

Who doesn’t like free stuff? Many credit card companies will offer new students a variety of “free stuff” to sign up for a credit card. There are many opinions about credit cards: some people say you should only use them in an emergency and some people buy too much and go into debt. Below, I’ve included lessons you’ll need to make sure you know how to use a credit card to benefit you. A credit card is a monthly loan from a bank. On my first secured credit card, I had a limit of $1,000. That means that every month, my bank would pay for my card purchases up to $1,000. You can get cash advances up to a certain percentage (if needed, but there are usually fees). You are responsible for eventually paying for the costs on the card. Every month you’ll receive a statement of your purchases. You’ll need to pay the “minimum payment,” but you should pay the full amount. Minimum payments are a scheme. This 1:19 video will quickly outline an example of what happens when you don’t pay off your full balance. Basically, a credit card has an Annual Percentage Rate (APR) that is applied to any balance that’s carried over month to month. If you pay off your bill when it’s due, you will not have any interest added to your bill. For example, my credit card bill cycle runs from the 23rd of each month to the next. I have until the July 18th to pay off my bill that covers my purchases from May 23 through June 23. If I pay the bill off any time between June 23 and July 18, I won’t have any added interest. If I paid off my entire bill before June 23, my credit score wouldn’t budge because it wouldn’t look like I’m using any credit. You shouldn’t freeze your credit card in a block of ice. Maybe such drastic measures would work if you’re already in debt, but if you’re just starting your credit history then this isn’t great advice. For example, say you have three people who would like to borrow $10. The first person is your close friend, but you know she never pays you back even though you’ve spotted her before. The second person is your close friend who always pays you back. The third person is a total stranger that you’ve never met. In this case you’d probably loan money to your friend who will pay you back. In the eyes of a credit card company, people who never use their card (or pay it all off before the bill is due) can seem like a total stranger. If the credit card company don’t know your spending habits, how can they know you’ll reliably pay them back? If you consistently use your credit card for reasonable expenses, your credit score will shoot up much faster than if you never use your card. Keep track of credit utilization. This is the percentage of available credit you’re using across all credit cards. I’ve heard from multiple financial advisors and bank reps that a 30 percent utilization rate (using only $300 of my $1,000 limit) is a good cap. I prefer to hover around 10% if I can. But in an ideal world, you shouldn’t go above 30 percent. Get organized. Missing even one payment can do significant damage. Other than your entire balance being subject to your interest rate, you’re also hit with a $25 or $35 late fee. Your credit score will also take a hit. So remind yourself to pay your bill, whether that’s a calendar date, phone alarm or something else. Some credit cards can notify you when you’ve used the card. Keep track and make sure you aren’t going over your preferred credit utilization limit. Start now. Credit history accounts for 35 percent of your credit score, so getting a credit card your first year in college and keeping it for years will help you have a higher credit by the time you graduate. You can use the above lessons and others to keep yourself on the positive side of credit and to avoid having debt. Personally, I spoke with a bank representative to talk me through how to responsibly use a credit card. If you can, I suggest you request a free appointment with them. Please let me know in the comments if you have any other questions or advice about spending!

0 Comments

Ask the right person.

There may be some teachers who you really look up to. But if you never had a meaningful relationship or did not do well in their class, then they may not be able to write the kind of recommendation letter you want. Carefully choose someone who can speak to your strengths that you want to highlight in your application. If you want UNC to know about your local community service, ask your nonprofit club advisor to recommend you. If you want to focus on your international interests, ask your favorite language teacher. Just make sure their recommendation can speak to the strengths you’re highlighting in your application. Ask now. Teachers have a lot to do over the summer and so many seniors will leave this request until this fall. If you ask now, your letter will be on the top of their to-do pile and they have all summer to craft a strong recommendation. Ask in person. This is the polite thing to do. Asking in person will also help you answer any immediate questions they may have, and will prove to them that you’re as serious about this recommendation as they will be. Give them a head start. Even if this teacher was your mentor all through high school, they’ll need some general information when writing your recommendation. I suggest you hand them the following once they accept your request:

Only ask for how many you need. If you only need two references, please only ask two professors. If one says no, then ask another. Please don’t ask for more because you won’t use them and that’s a waste of their time. Offer a delicious thank you. Bake him an apple pie. Make her chocolate-covered strawberries because they’re her favorite. Buy his favorite candy with a nice card because you don’t know how to bake. Do something special as a thank you because this person is helping you apply to college. They deserve something sweet. Do this only after they have written the recommendation. Follow up with your final decision! Tell them where you got accepted or where you committed to when the time comes. They are supporting your admission, so they’ll be interested in where you end up especially if their letter helped you get into your dream school. If you have any other tips, please share them below! Top Tips For Visiting Colleges

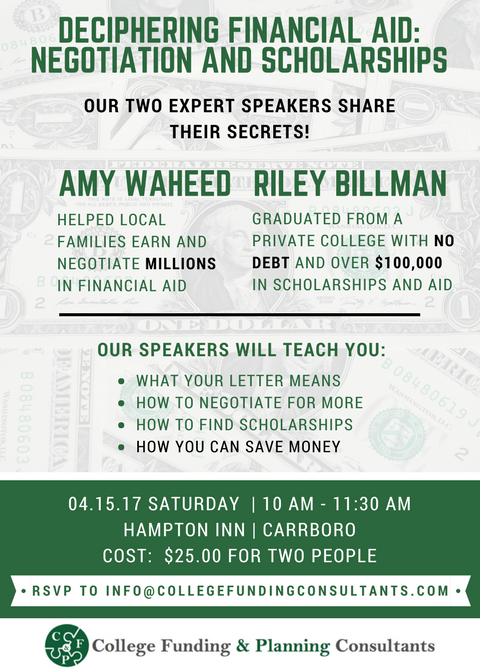

What’s your best tip for what to do on a college visit? Comment below! Hi everyone! Thank you for supporting my blog. I have an exciting announcement: I'm coming back to Chapel Hill! Only for a weekend, but still. I'm speaking at an event hosted by College Funding & Planning Consultants. I'll be talking about how I gathered over $100,000 in scholarships and grants, my negotiation tactics, and I'll even share my best tips to save money for college. I'm so excited to share all I've learned with you. I've included the invitation below for you. If you want to attend, RSVP to [email protected]. I can't wait to see you there! Feel free to let me know if you have any specific questions you want me to answer in my presentation.  I guarantee that this title isn’t misleading.

I knew that I wanted to graduate early before I even graduated from high school. To make sure I had the most flexibility, I wanted to make sure all my classes counted for as much as they could. I only took four AP classes, but they saved me from paying for an entire semester of college. Colleges have various required courses for general education (referred to as “gen eds”). Different schools can include a gym class, health, language, math, lab science, history, english, or a combination of others. Some AP class credits can count as these courses. For example, my AP Literature class counted as a literature elective class, so I didn’t need to take that. I also took BC Calculus, and because of my score the credits counted as AB and BC Calculus, which translated to Math 151 and 251. AP US History counted as HST 121 - US History Through 1865, which satisfied my history requirement. AP Comparative Government counted as an POL ELE (elective Political Science course). Since Elon operates on a four credit hour system and each class is four credit hours, I came into college with 20 credit hours. This was a great deal for a variety of reasons. First, I had more credits than most of the incoming class, so when I had to register for classes in the spring, I got to register before most of them because Elon opens your registration chronologically from who has the most credits to the fewest. Second, I got to take a class in my major and minor during my first semester. I didn’t have to only take the gen eds, so I got to see if my major was right for me on my first day (it absolutely was). My first day was an 8 am COM 100 class, and that professor became my academic advisor and an amazing mentor. Third, I had so much flexibility. I could take other cool gen ed classes that were exploratory but still counted towards my major. These classes usually fill up early, but I could get into them because of my credits. Astronomy counted as my lab science (before you laugh I spent over 8 consecutive hours studying for that final, and I guarantee it was one of the hardest finals I took). I took an intro to religion course, and American Philosophy. All of these counted towards my gen eds, but they helped me explore other areas. This is especially helpful for people still deciding on their major. You have room to take the exploratory classes that really interest you (and satisfy requirements) instead of whichever classes have one spot left when you register. I know AP tests are expensive. But college is more expensive. I remember the $93 test fee felt so expensive, especially when you’re taking multiple. But at Elon, one credit hour is $1,077. Remember, that’s not one class. That’s one credit hour, and one class is four credit hours. So one semester-long single class at Elon was $4,308. When you have a Tuesday/Thursday class that only meets 27 times in a single semester, that means each session of my class cost me $159.56. That’s more than a single AP test! Which got me out of the $4,308 price tag. I know it’s crazy. It sounds unreal. But it’s true. AP tests are an amazing way to save money in college. Now each school does AP test conversion differently. Most universities operate on a three-credit system, so each class is three credits instead of four. Some schools only accept a 4 or 5 on the AP exam in order for them to count. Some schools don’t accept certain exam scores at all. Make sure you know how your schools accept tests. If you’re still in high school next year, make sure your classes and exams could really transfer to college credits. If you’re about to graduate, make sure you know if you just need a three, or if you need a 5. If you have any other thoughts on AP exams, feel free to comment below and share your thoughts and advice! Let’s say you’re saving money for college. You keep it safe in a bank, you don’t touch it, and you know you’ll have it safe to spend on any of your college expenses. Sound about right?

Wrong. Here’s why: as a student, your assets are included in your FAFSA application, and can actually make a difference in your financial aid awards. This makes sense in theory, because if FAFSA pulls from your parent’s or guardian’s income to pay for college, they should do the same for the income and assets of students since they are the ones actually attending school. However, there’s one huge difference in theory and practice. This sounds nice, until you realize that a student’s income and assets directly add to your EFC. As we know, your EFC is the number that financial aid offices use to determine your financial aid award amount. The logic behind the direct addition to the EFC is that a student typically attends a college for four years. Since this hypothetical student should exhaust all their personal funds to pay for school (yes, this is actually the way it’s calculated), 25% of a student’s income and assets should be directly applied to the EFC. Yes, you read that right. Here’s an example. My first year of college I expected I would qualify for a Pell Grant because of my family’s limited financial assets. To qualify, your EFC must be below $5,920 (which is subject to change). My FAFSA EFC in 2013 was $9,409. I found that the only reason it was above the limit for the Pell Grant was because my mom took money out of her retirement for my college expenses so that looked like extra income, and my $6,000 in my savings account directly added $1,500 to my EFC. Those savings were all going to be used in my first tuition payment, but they were half the reason I wasn’t qualified for thousands of dollars of aid! Thankfully, there are ways to make decisions that influence your EFC more favorably. To be clear: you should never omit information for FAFSA. That would be a crime. But there are a few things you can do! For example, use those savings on material objects that you need anyway. For example, buy your laptop or dorm items before you apply for the FAFSA. Or choose that time to buy a car. Just understand that $0.25 of every single dollar to your name is going directly to your EFC. If you have any questions or other ideas, feel free to share! Google will give you 72,800,000 results when you search “what to bring to college.”

You don’t need that much stuff. I promise you. It’s very easy to get swept up in the excitement of college that you end up buying more than you need. But if there are so many ways to get cheap and awesome things. I spent most of my senior year compiling stuff for cheap so by the time I moved in, I’d already gotten most of my items. So here are a few tips to save while you shop for dorm room items! Look around the house. You probably have a lot of stuff in your room already that you can simply reuse. I brought my comforter even though it was technically a full size, so I just bought twin XL bedsheets. I used ottoman and all my desk stuff. I know it’s a time to reinvent yourself, but you don’t have to buy a trendy throw pillow right now if you don’t want to. Strategically ask for gifts you’ll actually need. If you know that you really want a new laptop, a piece of art, a printer, or any other expensive thing, ask for it for a birthday or holiday. You can tell different people different things, or everyone the same thing for a huge purchase. My friend spent a year asking for only Apple gift cards so she could save up for a laptop. If you know what you want to buy, try asking for it from others so people can get you things you’ll really use. Take advantage of thrift stores. Even Macklemore goes thrift shopping. This is the best place to get some of the random things you need. For example, you’ll probably only need one or two plates/bowls/cups/sets of silverware for your first dorm room. You can buy each for $1 at a thrift store, and pass them down to your siblings or donate them when you’re done. Ask siblings for stuff. If you’re lucky enough to have an older sibling, ask for their stuff. If they had plates or twin XL sheets, ask for them! As I went through school, I kept giving my siblings things like my single plates and cups, to an entire set of pots and pans when I left my college apartment. Bring one season of clothes at a time. Okay, you don’t need a tank top in winter. You don’t need snow boots in May. Only bring a season of clothes (and a couple extra things just in case) at a time. This can help you save on storage or shipping. You can always switch out your wardrobe during breaks or visits home. Always ask your roommate what they’re bringing. I kid you not, I know a pair of roommates who both showed up with a futon on move-in day. They didn’t know what to do, so they had two futons in their room all year. So please ask your roommate what they have and what they want to bring. If they already have a mini-fridge, don’t buy one. If you have a TV, bring it so they don’t buy it. It saves you both and makes splitting things at the end of the year very easy. Avoid the superstores on move-in weekend. They all know that the college students are arriving then. It’s an absolute madhouse. Bring everything you can and save your first trip for after that weekend. If you’re lucky enough to move in early, get everything you can before everyone else arrives. If you’re traveling far to school, I wish you luck. Once you get there: get the free stuff! Move-in weekend usually has lots of branded giveaways with cups and shirts and other things. Also, at the end of the year, hoards of college students give away the stuff they don’t want to take home. We decided to designate our laundry room as the area to offer up free stuff to your neighbors, and then the RAs donated everything that wasn’t gone when finals were over. I got so much stuff that I still use now. Anticipate your extra costs. Do you really need your car? Sometimes it’s really easy to get by without one. Since parking passes can get expensive, make sure you know if you need to bring it before just bringing it. Your room may already come with cable, so you may not need to splurge for that. Do you have any ideas for scoring cheap stuff for a dorm room or college? Comment it or share it with me in a message! Hello! Life has been crazy recently as I’m sure it has been for many of you. As some of you know, I recently started my full-time job in Washington D.C. I moved up here with my car full of stuff, and it’s so nice having my own apartment. Fun fact: life is really expensive, especially when you live in an expensive city. I’ve been carefully budgeting for everything, and I realized that balancing my budget would be so much harder if I had student loans hanging over my head ( thankfully, I have none). So today, I wanted to share with you how to understand your financial aid package, so you can understand it, negotiate and end up with fewer loans, too!

Let’s start with some financial aid vocabulary: Grants: Free money that goes towards education costs. You do not have to pay these back. Usually, these are provided by a governmental organization, through a Pell Grant, or other grant. Scholarships: More free money that goes towards education costs.You don’t have to pay these back, either. These differ from grants because they’re usually provided by an individual, organization or the educational institution. The only real difference is where the money comes from. Both are free money that you don’t have to pay back, so both are good. *Grants and scholarships sometimes can only be applied to tuition, or housing, or a specific element of the bill. Make sure that you know what it can be applied to. Subsidized Loans: These are government loans to pay for undergraduate education, where the government pays the interest while the student is in college. So if you got a $3,500 loan your first year, your loan is still worth that amount when you graduate because the government paid the accrued interest. These are only available to students with need who fill out the FAFSA. Unsubsidized Loans: These can be government or private loans for educational costs. Whoever signs for the loan is responsible for all interest, that begins accruing once the loan begins. Learn more about the difference between these loans here. Federal Work Study: This one is tricky. A student may receive a $2,000 Federal Work Study Program (FWSP), but that does not mean you will earn that amount. Basically, this FWSP is the government providing an institution with money to pull from to pay you. However, students still work hourly jobs, you don’t magically make more because you have the FWSP. You’ll still have to find a job (some schools help with this, others don’t), and you’ll still get paid that hourly rate. Some on-campus jobs are only available to FWSP students, so it can help you get a job, but you will not earn this amount, so don’t make the mistake of counting that as a scholarship. It is not. Feel free to email me about this or comment below and I can explain further! EFC: Your Expected Family Contribution (EFC) was determined by the FAFSA. This is not the amount of money you’ll pay for the year. This is a number that financial aid offices use to determine eligibility for aid, by comparing it to Cost of Attendance. Cost of Attendance (COA): This is how much the institution costs with everything included (like tuition, housing, meal plan, fees) and then some more (health insurance, transportation, books, etc). Usually the cost of attendance is slightly exaggerated for most people, because some of those extra costs may not apply to you. I lived 45 minutes from Elon University, so transportation was relatively inexpensive. I’d rent used books on Chegg, Bookbyte or Amazon. Financial aid offices take the COA - EFC to determine your need. Some people have an EFC that’s higher than the cost of attendance, which means you have no need. WARNING: Schools vary on what they consider in the COA total. Some include room and board, some don’t. So please make sure you look at what that number includes. You don’t want to think you have it all figured out and realize you didn’t account for housing or a meal plan. First, look at one award package at a time. If you have multiple, you’ll eventually want to compare them, but you want to fully understand what each one means before you compare apples to oranges. Some schools have particular scholarships or programs that others don’t have, and each scholarship can have different terms (like being renewable annually or a one-time gift). So for your own sanity, start with one award letter. Once you fully understand it, look at the next one. Second, read it carefully. Sometimes award letters abbreviate loan to L., so you may not know it’s a loan (award letters are notorious for not differentiating the difference between scholarship aid and loans, so make sure you carefully look at this). I’ve included the questions I’d ask myself about each aid item on my award sheets: -Is this a scholarship, grant or loan? -Are there any terms tied to this aid? Do I need to keep a certain GPA, be a full-time student, etc? -Is this renewable every year, or a one time gift? -Is this merit or need-based? These questions are important because if your financial situation changes, your aid can change. My mom got remarried (yay!!) but because I now had two incomes in the household, that changed my need. Similarly, when I became a part-time student my last semester, my total aid was cut to ¾ because I was no longer a full-time student. So make sure you understand the situation and what you need to do so you don’t accidentally lose a scholarship. Third, call the financial aid office and confirm that you understand the award. I’m not kidding. If you’re going to make this huge decision, you’ll want to verify with the office that you have all the right information. If you call and tell them you want to talk through the award letter to make sure you understand it, they’ll go through it with you. If you say each item and ask each question I included above, you’ll have the right information. Personally, I didn’t use these calls to ask for more aid, because they need to know that you’re a great investment before they’ll offer any aid. A random phone call will not prove that to them. Fourth, repeat this with all the award letters until you have them all done, then compare them. Some private schools may have a higher cost of attendance, but may offer enough scholarships so the COA is cheaper than a public school. Remember, these award letters are not final. You can always negotiate! Which will be the topic of the next blog post. As always, if you have any advice or questions about the process, feel free to comment them or email me! I’m so sorry I haven’t posted in awhile! I’ve been busy, because I accepted a full-time job! I’m absolutely thrilled, so all the meetings and work associated with that (which I can talk about in another post) are thrilling. To tie in with my recent employed-ness, I decided to write this post about networking, and how you can use it to help you even as a first-year in college.

I know some people who are terrified of networking. Why? It can be scary to ask people for help. It’s hard randomly calling people for an informational interview when they know nothing about you. Why would they want to help you? This is the example I always love to use when I explain networking. Think of whatever organization or club you’re most passionate about. It doesn’t matter whether it’s a sport, club, or job as long as you really love it. Imagine if someone younger than you reached out to you and told you that they want to be a part of it too, and that they’re really excited to join, but they want your advice and thoughts first. You’d be honored to help someone become part of something that you love. When people work full-time, they don’t (always) interact with students as much. Plus, when a student takes the initiative to reach out to them, it’s always memorable. The sad truth is that we really need to be memorable. When most companies post a job, they get so many résumés that they have to sift them through an algorithm-powered system to weed out résumés without keywords and phrases. Often, this means only 2% of applicants get interviews. Especially for larger companies, humans may not even see the first cut of applicants. This is where networking comes in. Imagine you work at a company, and you’re hiring for an entry-level position. Imagine you get 120 résumés and applications for the one job. Imagine that maybe a few people directly reach out to you, but one person stands so far above the rest by networking like a pro. How can they do it? Start by identifying your goals. If you want to work at a global public relations firm, if you want to work the front office of a professional sports team, or any other goal, then use that as your motivation. Once you know what you want, it’s just a matter of getting it. I’ll use myself as an example. I knew I wanted to work at a global PR firm (I knew my first-year in college. It’s okay to not know immediately, but try to apply this knowledge once you do know. Or use it to help you figure it out!). I decided to search online for the top revenue generating firms in the U.S., and find the best rated ones. I found a few who met both criteria. Then I decided to set up some informational interviews. What is an “informational interview?” It’s an interview that you as a potentially job-seeking person conduct (yes you actually interview them, not the other way around) in hopes to learn more about a company or organization that the interviewee hopes to potentially work at. You can also do these simply to learn more about an industry. Forbes has an excellent article that details the process further. I conducted these by reaching out to people that were one “connection” away. Maybe they knew my parents, or were a professor at my university, or they graduated from Elon. If you have some degree of connection, you can use that to strike up a conversation. The whole point of these interviews is to learn more. So ask questions, about job-hunting advice or about how to transition to working full-time and you’ve just started a relationship! Also, professors are awesome. They have years of experience, and they’re literally paid to share it with you. Go to their office hours, and ask about their experience or about their advice or connections. You would be so surprised how willing people are to speak with you about their experience and advice. If you are still in high school, you can use informational interviews, too. If you want to go to a particular university, ask around if anyone has a parent who’s a professor and may be able to tell you about a program you’re interested in. If you’re working, see if anyone knows people at the company you want to work for. If you’re travelling, see if anyone’s done it and can offer advice. The best part of all of this is that you get interview practice. The stakes are so low because you’re just learning, but it helps you conduct yourself professionally. I think by the time I actually had my first internship interview, I had over a dozen “informational interviews” under my belt, which made me more comfortable and prepared during the interview. Also there’s me! I love interviews, and I’ve done plenty in college. If you want to interview someone about how to do informational interviews, I will happily do it. I write a blog about this kind of stuff, and I tell my friends about it all the time. Feel free to reach out to me on my contact page. I’m not even kidding. I will talk your ear off about this and you’ll feel so prepared. This was a bit longer than most posts. Can you tell I love networking? It’s amazing, because you learn more for yourself, and you stick out as a passionate candidate to companies. You’d be surprised how few people actually write handwritten thank-you cards after an interview, or how few people reach out as a first-year in college. Plus, when I wrote my final cover letter for my job, I could honestly say that I’ve been so interested in this company that I did informational interviews there three years ago, and I’m confident that not many applicants could say that. I promise it’s not as scary as it seems. If you start sooner rather than later, you’ll be able to feel more comfortable by the time you actually apply for internships and jobs. If you have any questions for me, please feel free to comment! I’d love to answer any questions. Or if you have any informational interview advice, please share it! $25,218 of debt is a lot.

You’d have to work a minimum wage job for 3,478 hours, 20 minutes and 38 seconds to pay that off. Actually minus taxes it’s even more than that. Unfortunately, $25,218 is the average student loan debt in North Carolina. But there’s no need to despair. The Free Application for Federal Student Aid is here! Most students ignore the application and just have their parents or guardians apply. But you, or your kids, aren’t like most students. I know I took a big part in the FAFSA process, and I felt so much more comfortable with my aid negotiations because I understood the process. I’ve included some tidbits of information that will hopefully help you feel confident, too! 1. Here’s The Lowdown On The FAFSA First, it’s pronounced like “Phaf-sah.” Second, it’s a long application that can take over an hour to complete if you put every number in line by line. You will need your income information and tax forms, and you’ll need those from your parents/guardians, too. If your family owns a business, or has investments, that information is necessary as well. There are many lists online of what you may need. 2. If You Don’t Have That Kind Of Time You can use the IRS Data Retrieval Tool on the FAFSA to automatically input most of your information on the application. You can only use this if you/your family already filed taxes for that year and the IRS has received all the documents it needs. This definitely saves time, but make sure you still double-check the data. 3. Why You Should Care After you finish the application, you submit it and it’ll spit out an Expected Family Contribution (EFC) number. This EFC is super important. It’s basically the government saying it can confidently expect your family to pay that much (per year) for your college expenses. 4. Why That’s Not As Great As It Sounds That doesn’t mean the government will cover all costs above that number. They send that number (and your FAFSA application) to a university’s financial aid office, and that office will determine your aid based on that number. 5. What Formula They Use It changes on each university/college. But here’s an example. Let’s pretend your EFC is $10,000, and annual tuition and fees for college is $25,000. The difference is $15,000, which your institution would consider “need.” Some institutions guarantee that they will cover 100% of need, and some cover less. 6. Why That’s Still Not Great Your “need” is not covered by aid and scholarships alone. There is no publicly known formula for what percentage of that “need coverage” is loans and how much is scholarships/aid. Even an institution that covers 100% of need could only offer you lots of loans, or an institution that covers 10% may give you a $1,500 scholarship. 7. Why You Should Still Care About The EFC The lower your EFC, the more scholarships, aid and loans you will qualify for. You want to (legally) do what you can to minimize your EFC as much as you can. Because the formula is so complex, your EFC can be significantly impacted by a bunch of different factors. Knowing these factors can be crucial to maximizing your aid package. 8. Why You Want To Qualify For Loans Usually, federal loans have better interest rates and more long-term benefits than private loans. Also, federal loans come in two types: unsubsidized and subsidized.

9. Your EFC Is Not Set In Stone Fun fact: financial aid officers can adjust your FAFSA numbers if you have any new information, or corrected information. They can also adjust it to change your aid. So don’t feel like finishing the application is final and there’s nothing you can do about asking for more aid. You and a financial aid officer can talk about your situation and can adjust things, if possible. 10. Don’t Do It Alone Just like you go to a mechanic to solve your complex car issues, you should look for help and resources to help you with your FAFSA process. You want to make sure you've input all of the information correctly and you want to make sure you've made financial choices so you'll get the most financial aid that you can get. College Funding Consultants understands the complexities of this college maze. They help families with the process to maximize any aid you can receive and pay for college as comfortably as you can. Personally, I earned most of my financial aid through FAFSA adjustments and negotiations with the financial aid office. To me, being able to understand the FAFSA is absolutely necessary to getting as much aid as possible. I definitely recommend working with College Funding Consultants, because their team knows the formula and how it changes each year. Since you have to fill out the FAFSA each year you’re in college, you can either take the time to learn the formula yourself, or find people who can help. If you have any questions for me, please feel free to comment! I’d love to hear your FAFSA organization tips. |

AuthorHi, I'm Riley! I graduated from college in December 2016, after working to earn over $100,000 in scholarships and aid. Archives

July 2017

Categories |

RSS Feed

RSS Feed